Signs that a loan could turn into a financial headache.

Advertisements

Taking credit requires caution because A loan can turn into a financial headache. if you ignore the real impact of interest rates on your budget.

Often, the excitement of immediate profit blinds consumers to complex and dangerous contractual clauses that increase the final cost.

Before signing, analyze the real impact of the installments on your net income. This will prevent you from compromising your family's basic essential expenses.

Monitor the Total Effective Cost (TEC). There's something unsettling about how fees, embedded insurance, and hidden taxes go unnoticed in addition to nominal interest rates.

Knowing the institution's background helps prevent common market frauds. This ensures compliance with credit regulations stipulated by the Central Bank.

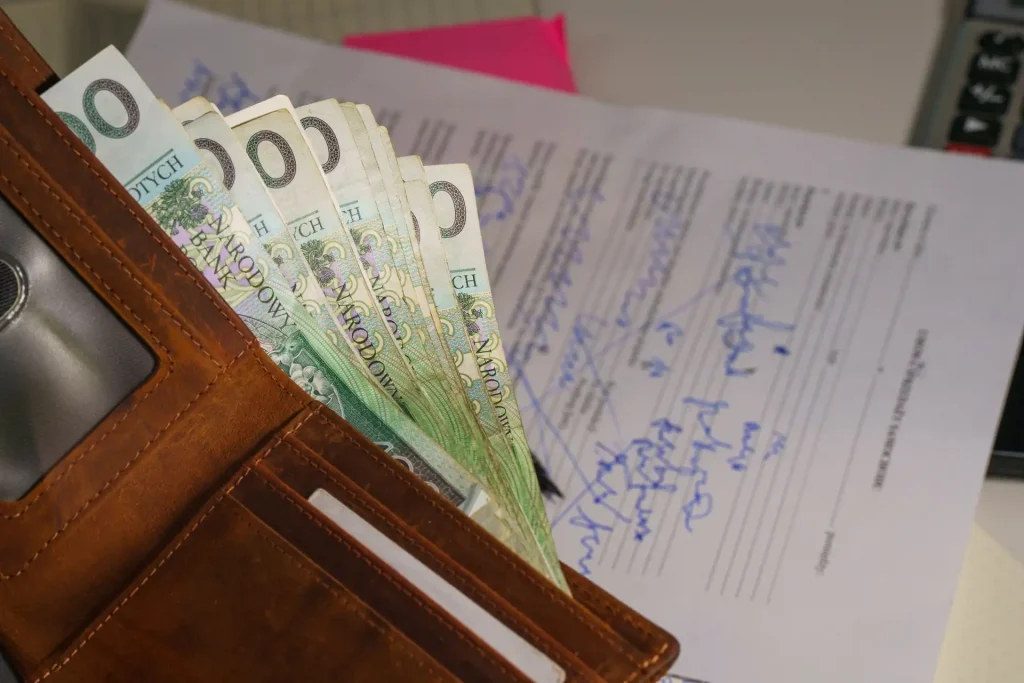

What should you consider before signing the contract?

The first visible warning sign appears when you need to use your overdraft facility to pay an installment that has just come due.

At this stage, A loan can turn into a financial headache. Because the snowball effect destroys its economic stability very quickly.

The need to take out new loans to cover previous ones points to an imminent collapse in the management of your daily cash flow.

Frequent late payments for basic bills, such as electricity and water, confirm that the loan repayment has exceeded your actual financial capacity.

What are the first warning signs that a loan has failed?

Many people only look at the nominal interest rate. They forget that administrative fees and insurance severely inflate the value of the installments.

The CET (Total Effective Cost) represents the actual sum of all charges and expenses involved in obtaining any type of current bank loan.

When comparing different offers from financial institutions, always request the CET (Total Effective Cost) spreadsheet to identify which option is truly the most advantageous.

Ignoring this indicator means you'll end up paying double the originally contracted amount, without realizing the impact of these accumulated extra charges.

How does the Total Effective Cost affect your wallet?

Excessive interest rates occur when the rates charged significantly exceed the market average officially published by the Central Bank for that specific period.

To verify this practice in reality, consult the official website of... Central Bank of Brazil and compare the percentages in the contract.

If the charges are incorrect, the consumer has the legal right to request a contract review through direct judicial or administrative channels.

Excessive charges disguised as operational fees also constitute abuse. They violate the protection standards of the Brazilian Consumer Protection Code.

When do abusive interest rates start to take effect?

Self-employed workers with fluctuating incomes face significant difficulties in keeping up with long-term, fixed payments.

Families that lack a structured emergency fund face financial collapse in the face of any unforeseen health issue or unemployment.

In these unstable scenarios, A loan can turn into a financial headache. by compromising resources intended for the daily subsistence of the family unit.

A lack of basic financial education increases the likelihood of taking out unsuitable lines of credit with conditions that are extremely detrimental to the household budget.

++ Comparing loan rates in Brazil: when is it worth paying less?

Who suffers most from excessive debt?

The table below presents the main average interest rates practiced in the Brazilian market in 2026 for different credit modalities.

| Credit Modality | Average Annual Rate (2026) | Operational Risk Level | Impact on the Budget |

| Public Consignment | 22% to 28% | Low | Controlled |

| Personal Credit | 60% to 120% | Average | Moderate |

| Revolving Credit Card | 400% to 450% | Most High | Critical |

| Special Check | 130% to 150% | High | Serious |

What is the ideal percentage of income for installments?

Financial experts recommend that the total value of all your loan payments should never exceed thirty percent of your total net income.

Setting aside a larger portion compromises the flexibility of your budget, preventing you from paying for seasonal expenses or investing in private retirement plans.

Keep an up-to-date spreadsheet containing all fixed expenses to visualize the real impact of new debt on your daily family routine.

Respecting this percentage limit ensures stability and prevents unforeseen events from forcing you to seek emergency resources that are much more expensive.

++ CHow to get loans with fast approval even if you have a negative credit history.

How to identify hidden fees in the contract?

Request a summary sheet of the contract and look for hidden terms such as tied selling, unsolicited insurance, and extra fees.

Many financial institutions include credit protection insurance without the client's explicit consent, illegally increasing the financed amount in the proposal.

Charging registration fees is only permitted at the beginning of the relationship; it is considered abusive if repeated in credit renewals.

Analyze each line in detail, because A loan can turn into a financial headache. due to these small, hidden monthly additions.

Why is credit portability advantageous?

Portability allows you to transfer your current debt to another financial institution that offers significantly lower interest rates and better terms.

This operation is free and regulated, making it an excellent alternative to reduce the total cost of installments that have become too burdensome.

When requesting the transfer, the new institution settles the outstanding balance with the old bank, initiating a new, more advantageous contract.

Research market conditions before negotiating, ensuring a real reduction in the Total Effective Cost of your new banking transaction.

++ Even someone with a clean credit history can have their credit denied? Understand why.

What are the dangers of revolving credit?

Revolving credit on credit cards is considered the most expensive line of financing on the market, generating astronomical interest rates in just a few days.

Using this resource to pay installments on previous loans creates a destructive financial trap that is difficult for the consumer to overcome.

The accumulation of compound interest transforms small debts into unpayable amounts, resulting in your name being added to credit blacklists.

If your bill is high, opt for traditional installment credit lines, which have considerably lower interest rates than revolving credit card debt.

When is it worthwhile to refinance debt?

Refinancing is feasible when the current institution offers a reduction in the interest rate or a healthy extension of the repayment term.

This strategy helps to lower the monthly payment amount, immediately easing cash flow, but it can increase the final total cost of the debt.

Assess whether extending the total term will make the debt perpetual, generating prolonged financial and emotional strain over the years.

Calculate the final APR before signing the refinancing agreement to ensure the switch brings real benefits to your wallet.

How to create a quick payoff strategy?

Start by listing all your debts in descending order of interest rate, prioritizing the payment of those that are growing most rapidly.

Allocate portions of extra income, such as the thirteenth salary and vacation pay, to pay down the principal debt directly to the bank.

Amortization reduces the contract term or the value of the remaining installments, generating a substantial discount on future interest charged.

Negotiate directly with creditors to obtain discounts for cash payments, eliminating outstanding debts from your budget once and for all.

Conclusion and Next Steps

Managing credit responsibly is the only sure way to avoid over-indebtedness and build a truly stable financial life.

Always remember to calculate the Total Effective Cost, respect the thirty percent margin, and monitor fees embedded in the contracts.

To better understand your contractual rights, consult the consumer protection guide on the portal. Federal Government Today.

Protect your assets by acting intelligently and strategically, ensuring sound credit choices that boost your projects without generating unnecessary risks.

FAQ – Frequently Asked Questions

How do I know if my loan has excessive interest rates?

Compare the rate in your contract with the market average published monthly by the Central Bank for the same type of credit.

What to do when payments are late?

Contact the lending institution immediately to renegotiate the term or request the transfer of the debt to a bank with lower rates.

What does it mean to amortize a debt?

This means paying off future installments in advance, directly reducing the principal debt balance and eliminating interest charges for that period.

Is the nominal interest rate the final value?

No, the final amount paid by the consumer is determined exclusively by the Total Effective Cost (TEC), which includes fees and mandatory insurance.